Australia’s goal of becoming a renewable energy export superpower is full of hope – and a fair dollop of hype – but a new report, funded by some of the industry aspirants, has underlined the numerous cost and industry hurdles that need to be overcome to make it an economic reality.

Australia’s unique geography is both its greatest strength and its biggest weakness – a near inexhaustible supply of some of the best and lowest cost wind and solar resources in the world, hobbled by its distance from many of the world’s major markets and the cost of transport.

For all the rhetoric of Australia becoming a green energy superpower – the “Saudi Arabia” of wind, of solar, of advanced minerals, or green hydrogen, or all of the above – there are already signs that some of the expectations around green hydrogen are being tempered by a dose of reality.

The Australian Energy Market Operator, for instance, is dialling down its new stretch scenario, hydrogen superpower, to assume less green hydrogen exports than previously thought.

That is a significant move because that scenario – however it might appear in coming years – is expected to replace “step change” as the most likely planning document for the transformation of Australia’s grid.

Last month, Mark Hutchinson, the new head of Fortescue Future Industries – the green energy vehicle of Andrew Forrest, the country’s richest and most optimistic green hydrogen evangelist – admitted that its big hydrogen deals with Germany may have to be met by resources closer to the target market, rather than Australia.

Last year, the UNSW-led HySupply consortium released a detailed report on the cost and supply challenges facing the country, which needs to overcome its geographic isolation that lumbers it with heavy transport costs, as well as the twin challenges of cutting the cost of electrolysers, and wind and solar.

The latest report shows that despite progress on many fronts, developing a new export industry at this scale is no sure thing, and it needs some showcase projects to show that it can be done, and to provide a path to tackle the cost challenges.

“The willingness of international buyers to pay for Australian exports of green hydrogen is still uncertain at this very early stage of industry development,” says the report prepared by UNSW and Deloitte, and featuring more than 50 interviews with some of the big industry players.

“(It) will largely rely on clarifying the preferred forms of hydrogen matched to end-use applications, acceptable green price premiums and appropriate embodied carbon emissions for ‘green’ imports to Germany.”

The stakes are extraordinarily high. Australia is likely to have a relatively big domestic demand for green hydrogen – as ammonia and fertiliser, in industrial uses and in heavy transport – but the big bets are being made on the export opportunities.

These include Forrest’s goal of producing 15 million tonnes of green hydrogen a year by 2030, a target that if delivered in Australia would require some 400GW of new wind and solar.

It seems an impossibility that that will all be built in Australia. Just how much of it is will depend largely on how quickly the industry can solve the principal cost challenges, secure a viable supply chain, and tap into government support.

One of the big take-outs from the survey conducted by UNSW and Deloitte is that the industry is sick of feasibility studies, and insists now is the time to scale up projects – with government support if needed.

“The only active electrolyser in Australia is a 1.25 MW electrolyser,” said one, referring to the installation at Tonsley in South Australia. “We need to commission electrolysers in the 100MW (scale), not conduct more repetitive feasibility studies.”

The report recommends that the priority should be on commissioning infrastructure and scale up to 300MW projects. “Many in industry are growing frustrated with repetitive hydrogen feasibility projects that provide limited practical experience for overcoming the challenges and uncertainties in green hydrogen export,” it notes.

Other issues are the lack of clarify over policy, regulation and incentives, and the need for government to step in with support for some of the early projects to help bridge the cost gaps, and cost of capital, identified in its previous reports.

“Australia is currently missing ‘show case’ projects that can act as an example for the market and encourage further investment,” the report says. It quotes industry players as saying “there needs to be a subsidy for the price and cost gap” and “something to encourage companies to go first.”

Last year’s report illustrated the challenge for Australia to grab a share of the green hydrogen export market, and beat the Middle East, north African and Latin America countries looking to do the same, and the efforts of customers – such as Germany, but also Japan and South Korea – to make green hydrogen themselves.

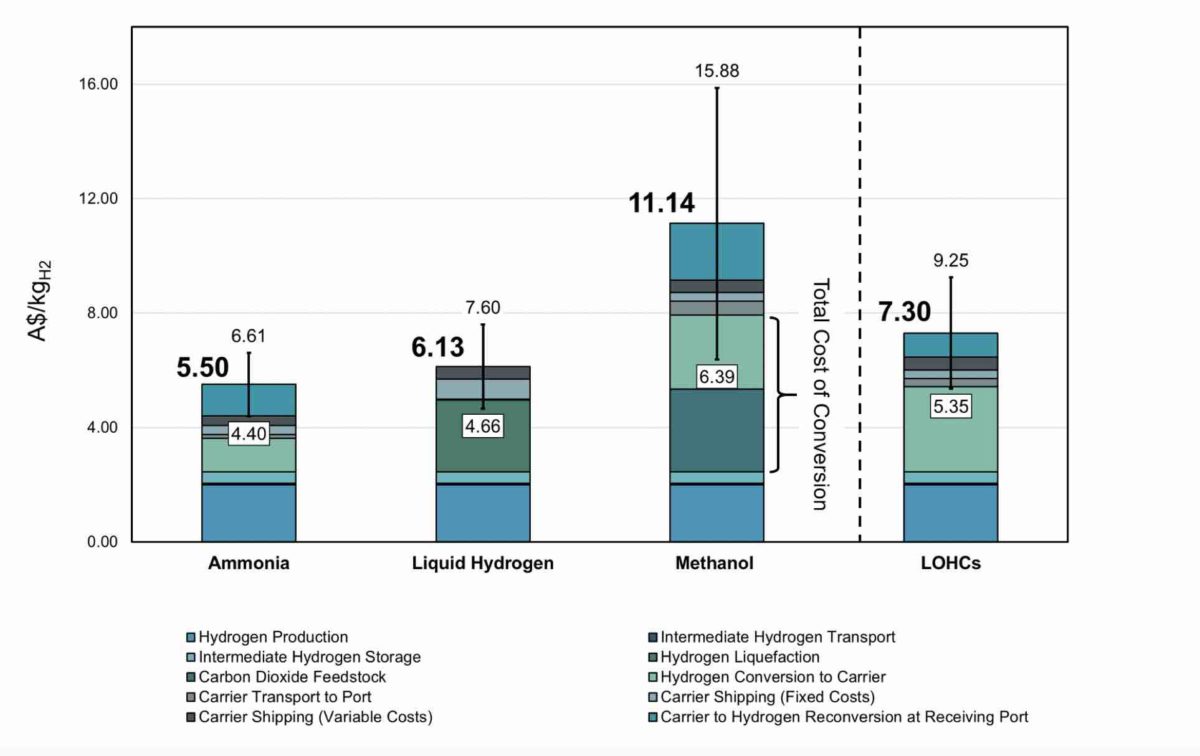

The first graph is the assumed cost of Australian delivered green hydrogen, from the cost of production to the cost of storage, transport to port, shipping, and conversion and re-conversion costs.

Even at these costs, there is one major caveat – and that is the assumption that green hydrogen can be produced in Australia at the federal government target of $A2/kg – considered the benchmark to make it globally competitive.

Australia is a long way from that now, and the HySupply report estimates that current costs are at least two or three times higher than that, possibly more. (It is impossible to say with certainty because there is so little green hydrogen production in place).

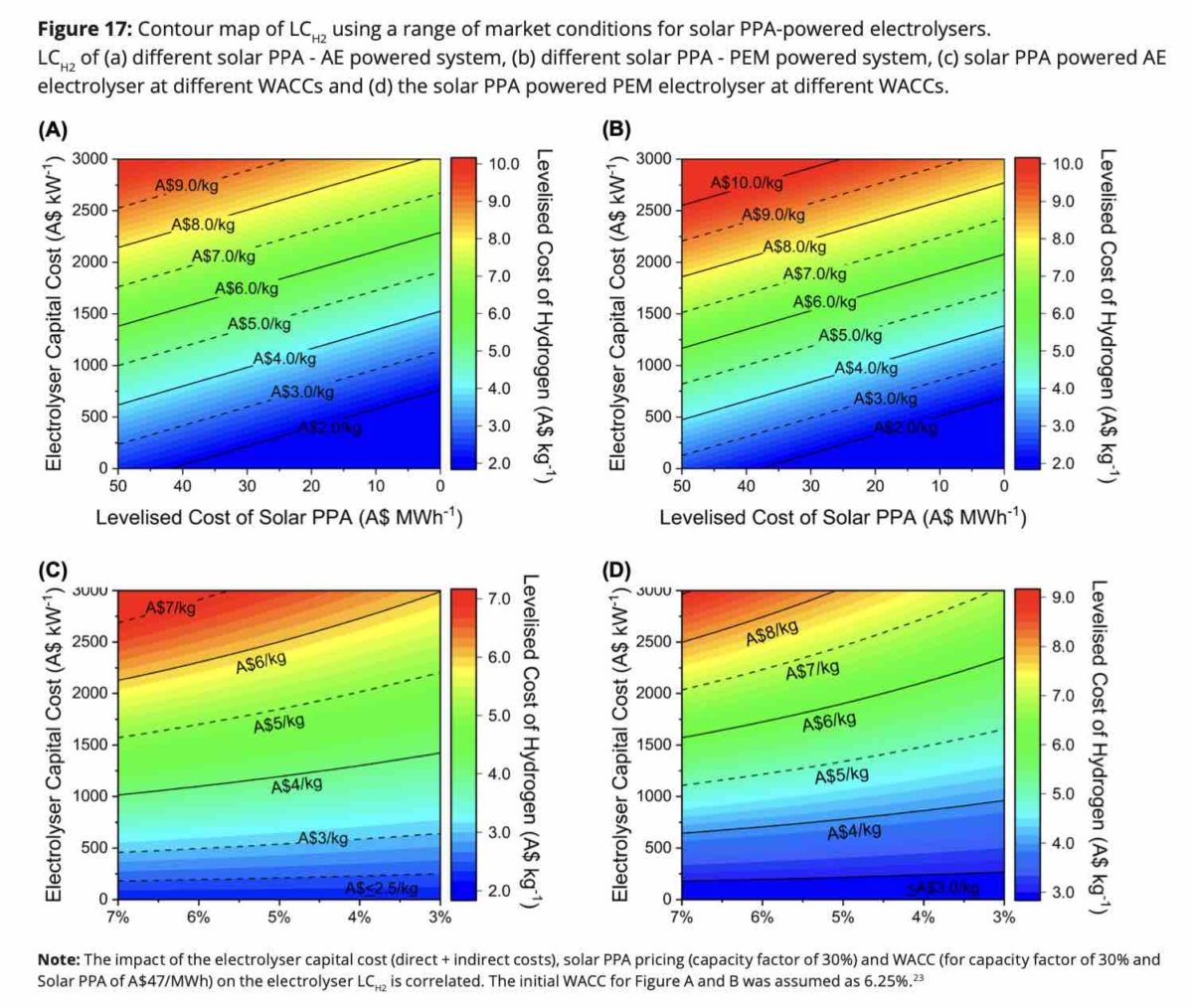

The key to getting the costs down include a rapid fall in the cost of electrolyser technology – from the current estimates of $A2,516/kW for alkaline electrolyser and $A3,510/kW for PEM electrolyser technology – to around $A600/kW. That will require it to follow the cost profile of solar, wind and batteries before it.

Then there is the cost of the solar and wind that will supply the “fuel” for the electrolysers, and a lot of this will depend – as it does with any technology with large upfront costs – on the weighted cost of capital, basically the rate that will be charged by banks to finance the project.

The HySupply members had already crunched the numbers in some detail.

A solar PV powered electrolyser (with a capacity factor of 30 per cent) ,and with a weighted average cost of capital (WACC) of 6.25 per cent, will require an electricity price of below $A20/MWh and an electrolyser cost of below $A500/kW to get to the targeted $2/kg.

Even if, in the long run, the electricity costs are reduced to $AS15/MWh (AEMO’s stretch target), electrolyser projects would still have to be financed at a WACC of less than 3%, and with a capital cost of less than $A500/kW to achieve the $A2/kg targets.

This graph above shows how the different cost assumptions change the equation and deliver the technology somewhere near cost competitive (blue).

The two two graphs combine the cost of electrolysers (on the vertical scale) and the cost of solar (horizontal) to deliver a levellised cost of hydrogen. On the left is alkaline electrolysers and on the right is PEM. Both graphs assume a cost of capital of 6.25 per cent.

The bottom two graphs show how different cost of capital can change the equation, and assumes a fixed price of solar of $A47/MWh.

The report is confident that electrolyser capex costs can reach the required levels by 2030, but less so about the cost of solar. It says this would need a reduction in the WACC of solar project from the current average of 6.25 per cent to less than four per cent.

The same principle applies to electrolyser projects driven by wind farms. Those financed at a WACC of

6.25 per cent will require an electricity pricing of less than $A30/MWh at an electrolyser capex of less than $A500/kW to attain a levellised cost of hydrogen of $A2/kg.

Wind projects would also need to be financed with a WAA of less than four per cent to achieve the $A2/kw target.