Sometimes in the National Electricity Market things suddenly turn off with absolutely no warning. This could be a generator, a load, or even an interconnector. Due to this we need capacity on stand-by to quickly step in when we lose load or generation to bring the grid back into balance.

Historically a lot of this stand-by capacity came from large generators that would leave wriggle room to quickly change their output up or down if needed. In recent years though we’ve seen batteries and even demand response begin to provide these reserve services too.

The Market Operator calculates then procures enough of these reserve through the contingency FCAS markets. Before October there were three ‘speeds’ of response procured:

- Fast: assets respond to a frequency deviation and ramp in a couple of seconds.

- Slow: assets ramp over a sixty second period.

- Delayed: assets ramp over a five-minute period.

The reason for these different speeds is so different technologies can participate in the parts that they’re best suited for. For instance, batteries may participate in the fast, slow and delayed services, whereas a large coal plant may primarily participate in the delayed service.

Due to the increased levels of variable renewables on the grid and a decreased proportion of thermal generation such as coal plants, imbalances in supply and demand sometimes need to be corrected even faster than in the past.

To accommodate for this new grid operating state there has been a new contingency FCAS service introduced: the very fast FCAS service.

The very fast FCAS service requires operators to respond in about a second to a fall or rise in frequency outside its normal operating range.

Consistently providing a firm response with one second of notice can be technically difficult or impossible for many technologies, so some NEM observers took interest in seeing which participants and technology types would operate in these markets.

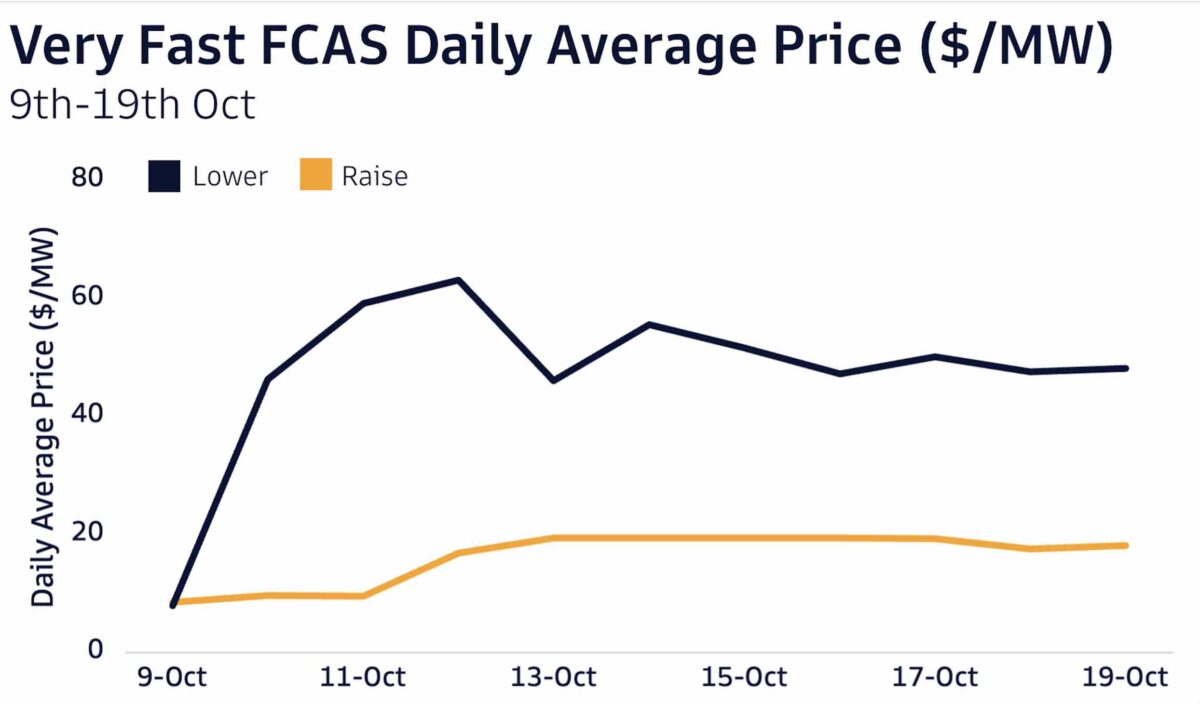

On October 9 the very fast FCAS markets commenced. The market operator tested the waters by procuring limited amounts, up to 50MW, with the upper limit to increase over time.

Over the first 11 days of operation $635,361 was earned by 9 participants. The majority of the revenue went to utility scale batteries, yet surprisingly almost 20% went to the commercial and industrial (C&I) aggregators EnelX and Viotas.

These C&I aggregators use high speed meters and control equipment to quickly adjust energy outputs at customer sites to provide the FCAS responses.

Almost all of the batteries that have participated to date are Tesla systems operated by Neoen, Iberdrola and Y.E.S Energy. The exception to this is the Queanbeyan BESS developed by Global Power Generation with technology from Ingeteam and Narada.

Many of these batteries were also supported with ARENA funding with the intent to provide new and sophisticated energy services which they have delivered on here.

While one must always be careful to not overanalyse small samples like this in new markets, one interesting outcome of the first 11 days is that prices for lower services were dramatically higher than raise services.

One reason why this is surprising is that raise required more capacity on average than lower at 50MW and 29.8MW respectively.

One explanation of this difference in price is that C&I aggregators EnelX and Viotas provided 60% of capacity into the raise markets. Theses aggregator bid capacity in at low prices, reducing the raise clearing price and undercutting a lot of the utility scale batteries in the dispatch stack.

As these aggregators utilise technologies like interruptible loads that can only provide raise services (by switching off during a frequency fall to contribute to raising the frequency) they had no capacity to offer into the lower markets, and therefore were unable to apply the same price reducing effects to that market.

Over the next few months as the market operator increases the amount of very fast services procured and more participants enter the market, this price reducing effect of the C&I aggregators will become less obvious. For now though, this presents an interesting microcosm demonstrating how DER can reduce the costs of running the electricity system.

This also demonstrates the technical and operational sophistication of some DER aggregators that can participate from day-1 in these cutting-edge services. Not only from the C&I aggregators but from Y.E.S Energy, who are participating with three 1MW batteries and generating revenue on par with much, much larger batteries.

And credit to the utility scale batteries for being accepted into the markets and will be playing a larger role as the capacity requirements of very fast FCAS increase.

On a final note, who pays the $635k that participants earned in very fast FCAS? It’s a mix of loads and generators, but large generators and loads pay far less than they should.

This leaves large costs unfairly (and inefficiently) borne by consumers, small businesses and small generators. Grids Energy submitted a rule change earlier this year to move contingency FCAS costs to a “causer pays” arrangement, which more fairly allocates these costs.

Mitch O’Neill is an independent consultant at Grids Energy, providing policy, strategy and modelling services to DER companies, governments and distribution networks.