Think, for a moment of the National Electricity Market as a human or a plant, where the parts contribute to the whole. The NEM is neither human not plant, and is in fact the country’s biggest machine. But if you assume transmission is built, there are no other significant barriers to building lots of wind, solar and batteries.

Chris Bowen’s newly expanded Capacity Investment Scheme is hugely significant. It may not get the country to its stated target of 82 per cent renewables, because of transmission and other constraints, but it is likely to get close.

The decarbonisation of the grid will proceed and the NEM will be at least 72 per cent renewable by 2030, and possibly more. As a result, prices in real terms will be lower, and it is a big blow to coal.

Before we get to more detailed discussion about the Bowen capacity news, let’s run through some other important assumptions, including demand forecasts and the state of the NSW planning regime, which is important because it affects the country’s biggest grid.

Demand

The Australian Energy Market Operator’s (AEMO) latest demand forecasts are summarised below. On the one hand, demand is expected to grow steadily after at least a decade where it didn’t grow at all. On the other hand, the growth is expected to be in non-traditional areas, like electricification.

It’s a much more nuanced picture than just plugging in population growth and GDP per capita growth. Even so, Australia’s population will grow by at least 1 million people between, say, 2023 and 2030, and they will all want to put the lights on.

Demand is more important and more difficult to forecast than supply, but despite the millions of words written about generation fuels next to nothing is written about demand or what it means.

One reason is that there are many experts (e.g. engineers) who know all about technology pluses and minuses, but energy demand is an obscure topic, not worthy of top economist insights and left to, say, AEMO and then commented on by humble analysts such as myself.

AEMO’s demand forecasts include many components and you need to read a detailed book to understand how they all fit together. Certainly, putting an Ikea kit together is easier than adding up the bits and pieces.

However, broadly speaking operational demand (the part supply by centralised generation) is expected to grow at least 10% by 2030, corresponding to a compound growth rate of 1.6% per year and total growth including behind-the-meter and hydrogen production could be double that rate.

I ignore hydrogen’s contribution to demand because the hydrogen facilities won’t be built unless the supply is locked in and they will offset each other.

The key point is that despite lacklustre growth in business demand, and the decline in residential demand supplied by centralised generation, overall centralised demand is expected to grow. But there are risks.

Aluminum is 20TWh of demand and needs to be repowered

There is the ever present possibility that Boyne Island, Tomago and Portland – with a combined consumption of say 20TWh – can close.

Repowering those smelters, given the forthcoming closure of coal stations in Queensland (Gladstone), Victoria (Yallourn) and New South Wales (Eraring, Vales Point) remains a national challenge.

Of course many of us have ideas about that, but here I proffer a view that looking at the smelters separately is a silly idea. If there is one overwhelming feature of a variable renewable energy (VRE) supplied grid is that it has to be looked at in both demand and supply terms as a portfolio.

It needs far more firming to supply a flat load smelter looked at in isolation that it does to supply the entire NEM. Firming raises costs. The less the better; albeit, the alternative is more transmission.

However a portfolio of variable renewable energy (VRE, essentially wind and solar) designed to supply a 1GW flat load in, say, NSW, needs far more firming than a high wind portfolio across the NEM that supplies 25GW.

I personally don’t think the corporates involved actually understand that, or even care. That, after all, is the government’s job, in their view.

And I’m not sure that governments, both federal and state, yet fully understand the benefits of the portfolio over the individual. And even if they did offer an intellectual nod to the concept, can they really do anything?

Supply

Despite the apparent gloom over new projects; despite the fact that the NSW Dept of Planning has become “Das Schloss” with the apparently not-so hidden goal of stopping wind and solar development, or at least making it as difficult as possible.

Despite the opposition of rabble rouser Barnaby Joyce; despite the fact that offshore wind is unsurprisingly turning out to be colossally expensive and almost totally unnecessary in Australia, and; despite the fact that governments are sold on the view that lots of long duration pumped hydro is required even though the ISP clearly shows it isn’t.

Despite the fact that European wind turbine manufacturers have chased rats up drainpipes and forgotten about the benefits of long production runs and now need higher prices to get back on a sound footing…

Despite all these things, the weight of the evidence suggests that wind and solar projects will continue to be progressed, developed and delivered and that the transmission will be there for the projects.

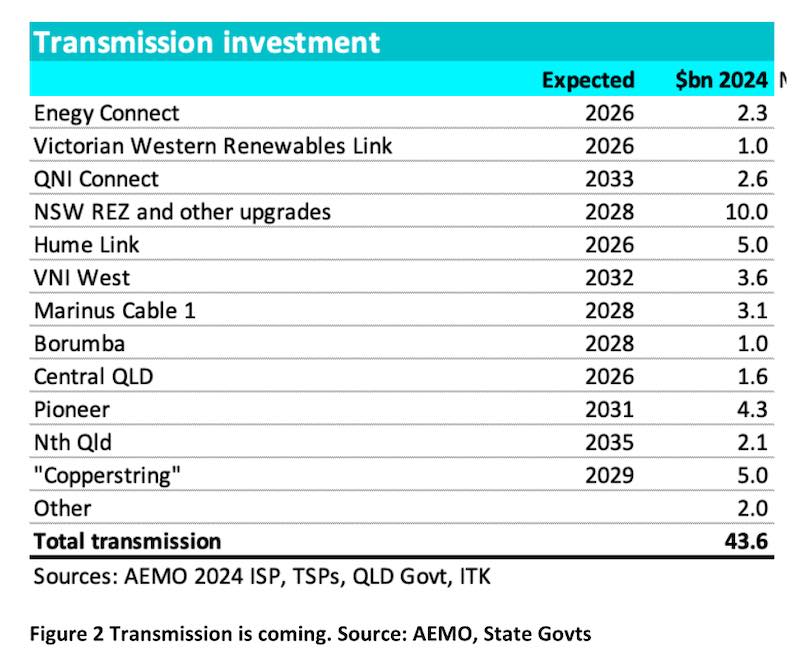

Start with transmission

The first draft of the 2024 ISP is scheduled to be released by December 23, 2023. However ahead of that, the new transmission build schedule I work to is:

Although $5 billion is a big number for Copperstring (Townsville to Mt Isa) and there is no demand to speak of in the area (400MW max), it’s a great wind and solar resource and in my modelling is heavily selected in a maximum NEM-wide “Sharpe ratio” portfolio.

Load is potentially available at Gladstone 1200km away, even if Mt Isa closes. However, the project is justified by the government as opening up the other North West province (the one in Queensland, not in WA) because of the strategic mineral deposits.

Although the Queensland government talks of 6GW of new capacity, a 500 kv AC single circuit has a capacity of 1500MW. On the face of it, Copperstring is utter overkill. However, I expect it’s a case of “build it and they will come.”

Still, the point is lots of transmission is getting built and the vast majority of it will be built by 2030.

Notwithstanding the social license issues – and I do take them very seriously – the fact is that transmission has been built in the past, land owners are significantly better recompensed than in the past and in the end the easement legal power will get the job done.

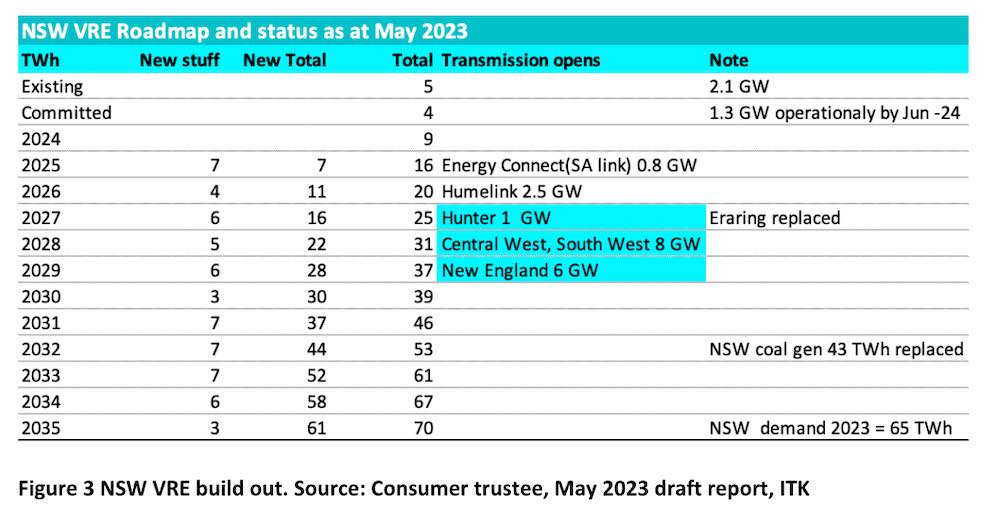

Next we can look at the NSW consumer trustee LTESA expected awards. Again it is not news to say that the LTESA payments do not justify a project, but in my view they are a good indication of what will get built and by when.

The obvious issue in this table is that the Consumer Trustee expects 5GW of new build to be operational prior to any of the REZ transmission upgrades being complete. So the question is whether there is 5GW or even 6GW of available capacity within the combined transmission and distribution networks.

I find it hard to believe that AEMO Services would make forecasts that could not be achieved. If AEMO Services didn’t think the new capacity could be connected or was dependent on transmission builds to the NSW REZs it would surely say so. But it didn’t.

The following is an extract from AEMO Services’ May 2023 publication. That publication discusses all the transmission augmentation that will impact NSW, so the generation forecasts clearly have considered the available transmission in NSW between now and the opening of the NSW REZ links.

Doing things differently has started slowly in NSW

NSW is effectively pioneering REZs in Australia. There have been plenty of mistakes and probably more will be made, but essentially from what I see as a spectator there have been three difficult areas.

1. A Dept of Planning that appears to be almost comically incapable

I can’t help but contrast what happened in Queensland 10 years ago when, not one but three LNG plants were built on Curtis Island; 1000s of wells drilled, the south-east Queensland transmission system rebuilt; and not one but three pipelines built to connect the gas wells around Roma/Chinchilla to Gladstone. This was all done over six years. Well over $60 billion of capital expenditure in the $ of the day, a lot more now.

In NSW, you’d be lucky to get one wind farm approved in that time, lost in an endless morass of studies. There doesn’t seem to be any whole-of-REZ planning. It’s unbelievably poor. An indictment on the prior, as well as current, governments. No responsibility taken, and a work to rule mentality.

It’s not working longer but working smarter that’s required. Coming up with solutions not problems. REZs geographic boundaries, an estimate of the REZ capacity and the required transmission capacity. But the worst student in a town planning class would do better.

Residents want to know where the wind and solar farms are and so much more. It’s a job for a planning department but not that excuse for a department in NSW that manages to put Environmental Impact Statement (EIS) bombs in the way of everything.

EIS is important, very important, but the department needs to show how it can contribute to what’s going on, rather than just providing lists of check boxes.

The department needs to help. The Secretary of the Department has only been Secretary for five months (acting secretary for three months prior) and indeed has only been in the Department of Planning for a couple of years (source: Linkedin). So clearly not much experience right at the top, when coupled with a new Minister.

Things like the recent infamous “no wind” map are to me indicative of a department that just is nowhere near the standard required. Frankly, I question whether the leadership team is up to the job. But maybe it’s about to improve – and hey, I’m just a spectator.

To reiterate, we are talking about well over $20 billion of construction that needs to be completed in the next seven years in regional NSW.

2. Developer doubts about the REZ GPS concept

Developers feel that this process has the potential to cause delay rather than improve the prospects of AEMO approval. Again, speaking as a spectator, it’s the least of the three concerns because there aren’t enough projects to require an REZ GPS as yet.

3. The new model of competitive transmission tenders

At the moment the issue seems to be that neither the transmission tender winner nor the users of the transmission line have enough confidence in each other to commit. Confidence is something that can be provided. In my view this is something that could be sorted out promptly. If it was, other things might start to fall into place.

The point is that despite the appearance of being hopeless, it remains perfectly possible – even likely – that there will be lots of new VRE built in NSW over the next five years.

The obstacles are not financial, not physical but a lack of management, a lack of confidence and a lack of people skills. Like a bad football team that gets the right coach a few poor seasons can quickly be reversed.

Elsewhere things are progressing. Queensland is cracking on, even Victoria is doing a bit, South Australia has enthusiasm. Tasmania has been slowed down by cutting MarinusLink in half, but nevertheless there will be more development there, for better and for worse.

ITK forecasts

ITK forecasts are actually a bit more aggressive than those implied by the Capacity Investment Scheme announced by federal energy minister Chris Bowen this week.

There are few details of how the scheme will work, and almost endless questions. One of them, relevant to forecasting, is what constitutes a “committed” project. Such projects are not eligible to participate in the scheme.

ITK greatly welcomes Minister Bowen’s initiative for at least two reasons.

Firstly, it acts as a federal backstop to state policy. It will tend to make the National Electricity Market more relevant, as opposed to each state doing its own thing. I’ve already said it many times, but a NEM-wide portfolio approach is likely to be the best – a NEM-wide approach that always understands and works hand in hand with distributed energy.

Secondly, the announcement supports my number one rule that science will drive policy. Conclusions from climate science continue to suggest that more and not less policy is needed. That is the best bet to understanding medium-term energy policy.

If we just add up renewable output over the last 12 months and the expected output from the new policy (I ignore the firming stuff as it is a net consumer of energy) I get to just over 70% renewables by 2030.

“Under construction” includes Golden Plains, about 3GW or more in Queensland and Uungula, Uralla Solar stage 2 and other NSW announcements, + a bit of South Australia.

These numbers were similar to my own estimates prior to this announcement (see below). My estimates took the NSW and Queensland schemes into account and various other guesses. Please note that this forecast is for 2028, not 2030.

Another blow for coal generation

Policy announcements are just that – announcements. They are not of themselves facts. Management has to come to a conclusion about whether the policy will actually eventuate.

If the market comes to believe, as I think it will, that 22GW of wind and solar will get built by 2030, then more coal stations will close. Vales Point will be in the firing line along with Gladstone, as well as the already announced Eraring and Yallourn.

Full analysis will have to wait.

Prices will fall

I think prices will fall in real terms, but it’s not just me. Here is the AEMO commercial price index forecast associated with their latest demand forecasts.

I don’t know how AEMO comes up with their forecasts but my reasons for expecting prices to soften somewhat are:

- Batteries will compete with each other and with gas for morning and evening peak prices.

- Midday prices will stay suppressed.

- Overall supply will grow faster than demand.

- Learning rate effects will eventually reassert themselves and drive down wind, solar and battery costs in real terms.